ai architecture

Credit Risk Modeling System Architecture

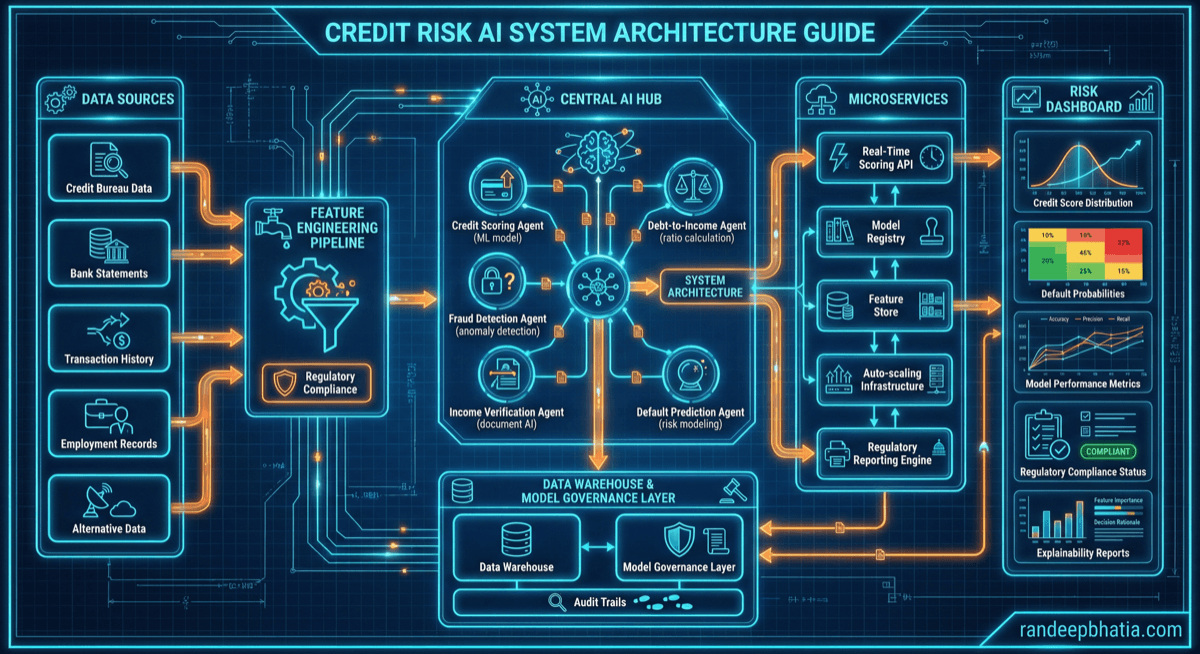

Production-ready system architecture for credit risk modeling. Includes component design, data flow patterns, scaling strategies, and security considerations.

2025-12-18

View Full Size

Production-ready system architecture for credit risk modeling. Includes component design, data flow patterns, scaling strategies, and security considerations.

2025-12-18